WasteCo Dumpster Fire

Or: The issue of listing on the NZX

A good piece in BD this morning on WasteCo, the tiny NZX-listed company that somehow can’t make a profit. Link here (paywalled), but here’s a sample:

On one side, Storm is backed by several shareholders in calling for the acting CEO and board chair, Roger Gower, to resign over the firm’s poor performance. They say the value of their holdings in the waste firm has been decimated, Gower is out of his depth, and his leadership is hurting the business. The board, which includes reverse-listing specialist Sean Joyce, backs Gower and says that Storm is fomenting discontent and has set up a new business to poach WasteCo staff and customers

You will perhaps recall that WasteCo was another reverse listing, with reverse listing specialist Sean Joyce at the helm (Joyce was also involved with the doomed Being AI, another reverse listing). When WasteCo listed the shares traded at 8c. The shares as of writing today are 0.7c.

I can point to a bunch of reverse listings where the same occurred — obviously Being AI is the most famous example (for my intl readers, Being AI was allegedly an “AI” company that comprised of a charter school, a mailing business, a filing cabinet storage business and a nebulous “AI” consultancy).

What I’m saying here is: is this another example of a doomed reverse listing? List a company — in this case a fairly easy to understand business — and then create a massive balls-up where you destroy shareholder value for everyone involved?

I have some sympathy for Storm and his co-founders (all have exited the business): you’re a fulla with a truck or two, you pick up rubbish, you build a business. Then someone convinces you to list and suddenly you’re making all these acquisitions, piling on debt, and the business you built is worth a tenth of what it was at listing. What were they thinking? Were they sold a dream? “List and you’ll be huge, boys”

In the wider context of the NZX it obviously is yet another case of a botched listing that makes it unappealing for prospective entrants to list.

Consider recent listings. Take My Food Bag, a meal kit service. Disaster since listing.

Or take WasteCo:

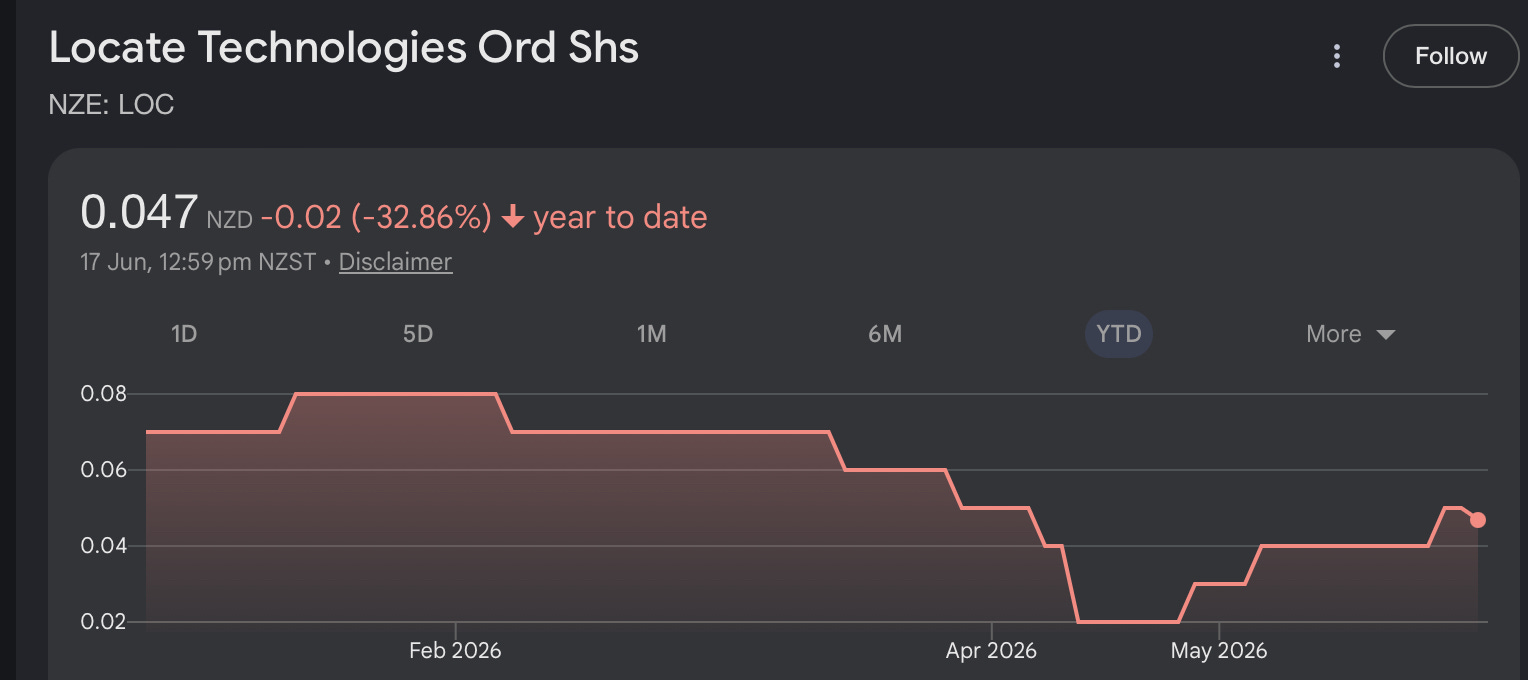

Or take Locate Technologies, the much-touted “bitcoin treasury” company:

See the issue? Why list? The NZX listings team must be powered by pure hopeium — “don’t worry, that won’t happen to you!” (And look, I sincerely would love to see more listed companies — but the current lot haven’t looked good).

Now, I’m sure the WasteCo boys were told they’d get access to capital. And they have! Recently they established a new $10m funding facility; they have undertaken multiple rounds of convertible notes; they have made acquisitions. And yet — I mean — had nobody told management (multiple senior staff have come and gone) or the board that you need to make a profit? As in, if you finance costs eat everything up, then, well, what’s the point?

Anyway — it seems like WasteCo’s issues are deeper rooted. The current chair blames Storm; Storm blames the current chair. There’s blame all around! The company is worth something like $8m — even in the world of small caps it is small.

I will level with you: it is my opinion that the company seems doomed. You’ve got a company with $70m in revenue and a $12m loss. Or take it from the company’s own annual report:

At the reporting date the Group had cash of $1.2 million (2025: $5.9 million), negative working capital of $28.7 million (2025: $4.0 million negative) and net assets of $3.2 million (2025: $15.3 million).

As at 31 March 2026, the Group had borrowings of $40.1 million (2025: $41.0 million) of which $26.7 million were current (2025: $8.7 million) and $13.4 million were non-current (2025: $32.3 million). Prior to the reporting date the Group identified it was likely to breach its equity and leverage ratio covenants in its bank facilities with Kiwibank as at 31 March 2026 (note 18.3). Accordingly, the Group sought a waiver from Kiwibank and received a conditional waiver on 31 March 2026.

The Group considered the waiver conditions were manageable, and the conditions of the waiver were satisfied shortly after the reporting date. Because the waiver was conditional at the reporting date the borrowings from Kiwibank are disclosed as current in the Statement of Financial Position.

Kiwibank’s subsequent confirmation of the waiver confirmed the original term of the borrowings.

The only way WasteCo gets out of this alive is somehow increasing revenue to the extent that they can break even. My rough back-of-napkin analysis is they need ~$104m of revenue to breakeven, or +48% of their FY26 level.

You have to ask yourself, is management and the board going to increase revenues by +48%?

If not, are they going to cut costs radically?

And what are they going to do about co-founder Storm and other disgruntled shareholders?

Frankly — it’s a hard task. If you’re a shareholder, you must be hoping for a miracle.