Salvaging the Tech Wreck

Is there any hope? Maybe.

I began to think about this question a couple of weeks ago, when a friend said “yeah, the tech wreck has sold everything off, but if you’re ballsy, there could be the opportunity to double your money on the right company”.

Another call with a friend this morning. We talked about Uber. As Citrini puts it here, AI agents don’t care about user loyalty. They’re going to shop for the best deal — whether it’s via Uber, or Waymo, or whoever. My initial response was “well, Uber has a network of x drivers in the world and it’s habitual for people to use Uber, so their moat is how embedded it is”.

But was I wrong? Consider and agent-to-agent future. You request a ride in your AI app (Chat GPT or whatever), and the ride request is sent to driver’s agents, who then bargain over the best cost. In this scenario Uber is decimated. It is zero. There’s no need for Uber because the agents are handling both sides of the transaction.

Obviously, this is why the tech selloff has been so brutal. Citrini puts it better and it’s well worth a read. And obviously, this is why Canva — as we talked about yesterday — can’t list anytime soon.

So we need to do some hard thinking. The most Munger-esque answer is to invert the situation: what industries aren’t affected by AI? That is to say, what industries don’t rely on connivence and then charging a fractional transaction cost.

Here’s some ideas.

Real products (yes, it’s alcohol again)

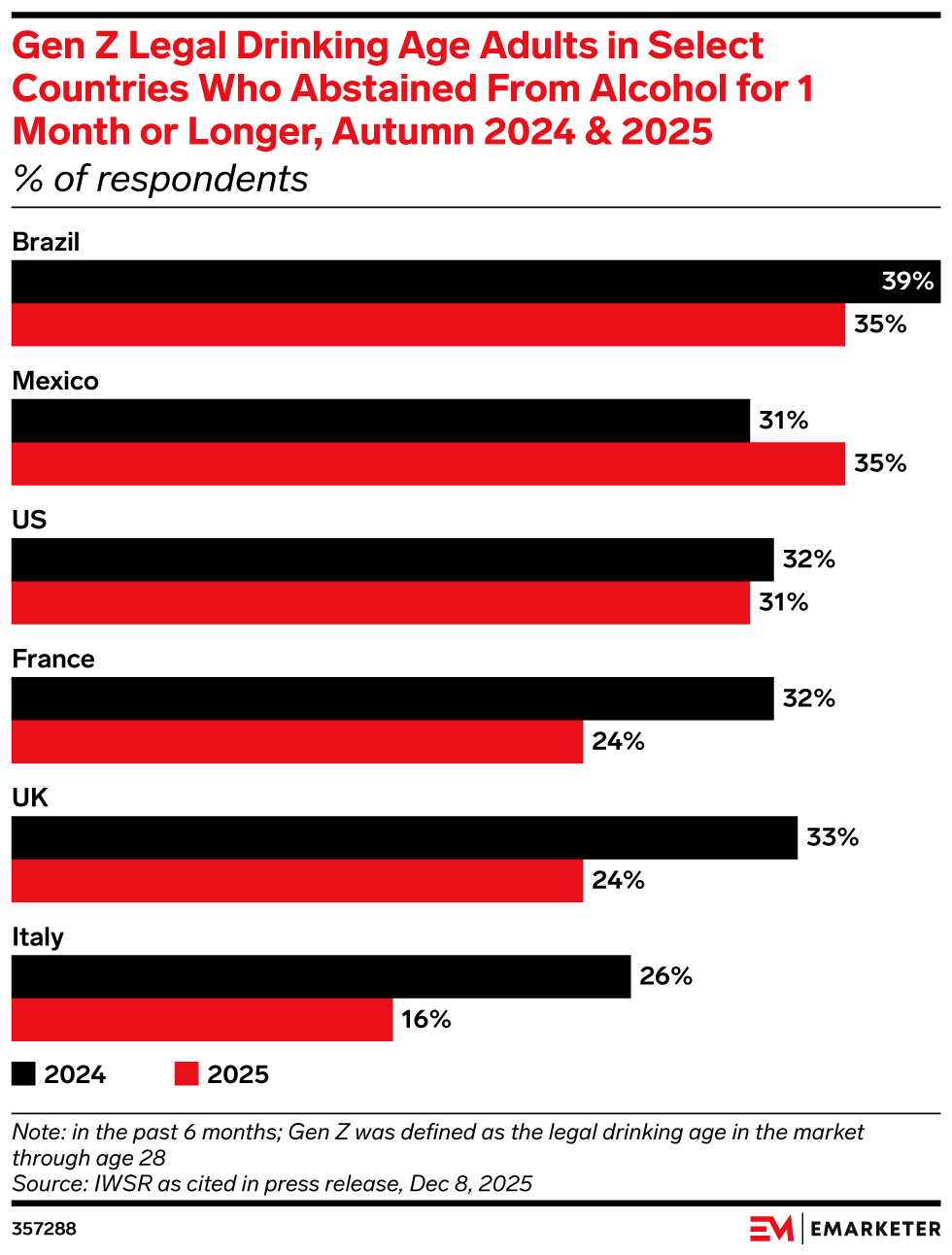

Everyone has been making fun of me for being long booze makers for some time. Gen Z aren’t drinking, everyone says. Which is not quite true… see the chart below. Gen Z non drinkers are declining YoY (no doubt as disposable incomes grow).

AI is not a threat to alcohol companies. AI does not drink alcohol. Nor is the value proposition simply “we take a fraction of the cost and act as an intermediary”. Alcohol is a real product and it is backed by thousands of years of human consumption in some form. It is simply dumb to imagine this will not continue.

Alcohol is a liquid. At this point I would like to borrow from Charlie Munger’s classic Coca-Cola parable:

We will next use numerical fluency to ascertain what our target implies. We can guess reasonably that by 2034 there will be about eight billion beverage consumers around the world. On average, each of these consumers will be much more prosperous in real terms than the average consumer of 1884. Each consumer is composed mostly of water and must ingest about 64 ounces of water per day. This is eight eight-ounce servings. Thus, if our new beverage, and other imitative beverages in our new market, can flavor and otherwise improve only 25 percent of ingested water worldwide, and we can occupy half of the new world market, we can sell 2.92 trillion eight-ounce servings in 2034. And if we can then net four cents per serving, we will earn $117 billion

Well, it’s the same logic with alcohol, except you get a “lollapalloza” effect because the substance is also addictive and occupies a unique place in our culture. People are going to consume some form of liquid a day; it figures that a portion of people will consume alcohol, and so on. None of this is “disrupted” with AI. The human need for liquid continues on, unabated.

Of course, the liquor industry has its problems. In the US there is the fascinating case of Uncle Nearest; in the wider scheme of things you have Dave Lewis, the new Diageo boss, grappling with a turnaround plan. But these are structural issues, largely. For years the liquor industry pursued small distilleries and so on, annexing smaller brands to their large conglomerates with little rhyme or reason. There is now too much wine, and too much spirit. The economics are elementary — if you have more supply than demand you end up lowering your prices. If you are a big company you can handle this situation (case in point, Jim Beam just closed their distillery for the year). If you are a smaller company you are faced with more of an existential crisis.

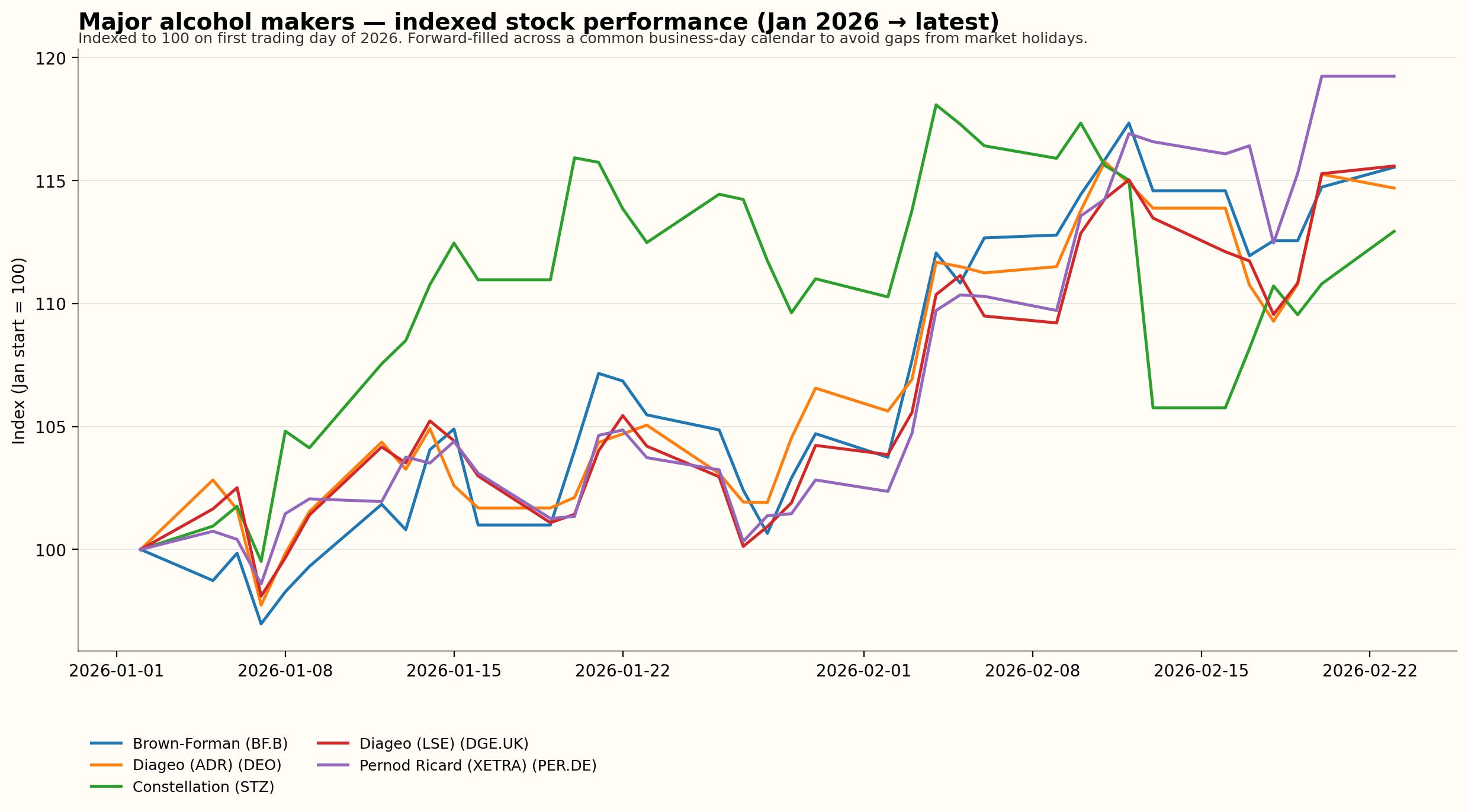

Yet, as with everything, supply and demand situations end up correcting themselves. There will be casualties. The “majors” — Brown Forman, Pernod, Diageo, etc — are insulated enough to ride it out. They’ve all had their stock prices walloped in the past few, post-COVID years, but it’s telling that all their stocks are up since the start of the year.

Of course, some of this is a symptom of needing to allocate capital somewhere. If you are a fund manager and you are observing the tech wreck, then perhaps you are going to move your FUM to consumer companies. Yet it’s also about reversion to the mean: alcohol stocks have been deeply unfashionable for years and it’s possible they have hit valuations that are so rock-bottom it’s hard to ignore.

Brown-Forman stock is up 15% YTD.

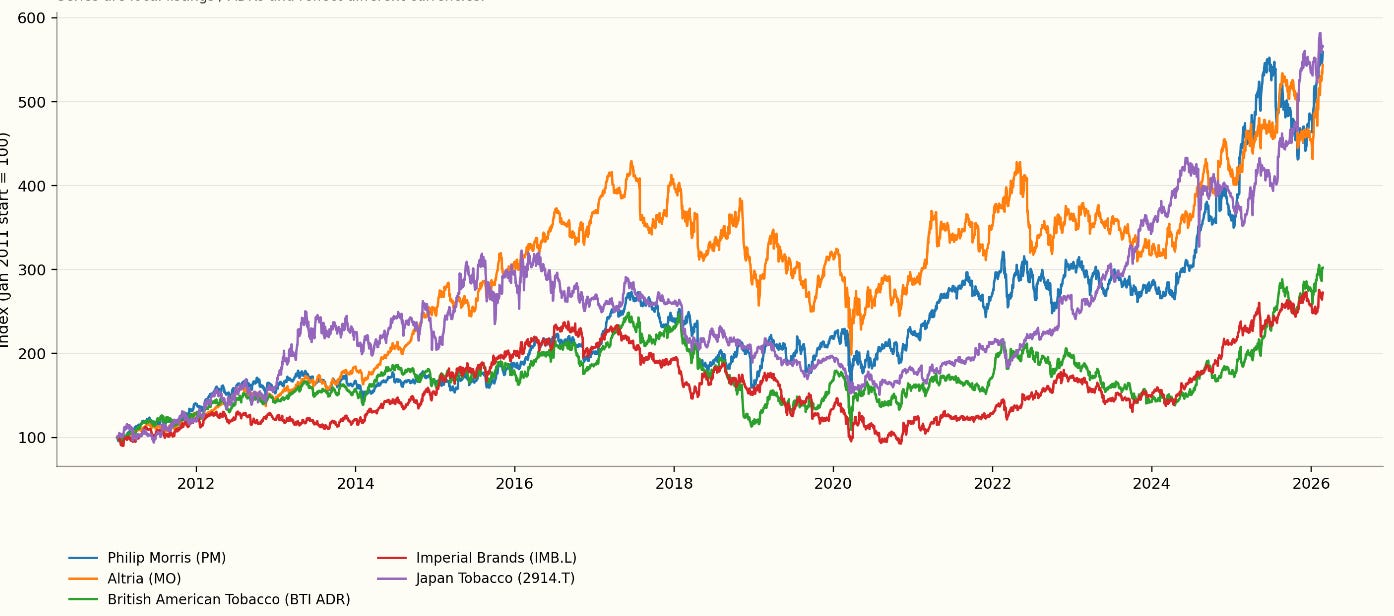

A little side note — the same occurred with cigarette and tobacco stocks some years ago. They were in the toilet. The rationale was similar to alcohol today: young people aren’t smoking! Yet over the past 15 years, those once-unloved stocks have steadily regained ground, as can be seen below.

Perhaps the prevailing wisdom, which always seems to be vaguely moralistic in its messaging (“smoking bad!” “Drinking bad!”) is incorrect. It’s my experience that you make the most money when everyone thinks you are an idiot (see: Kering).

Very boring companies

One of the most boring companies I know is Otis, who make and service elevators. The business is very simple: you buy an elevator from them, they service it forever. That’s it. That’s the business.

The overwhelming amount of profit made by the business is in the servicing segment. You can think of selling the elevators as really selling decades and decades of service revenue.

I will be the first to admit the business is as dull as dishwater. It’s not going to get anyone’s heart rate racing. And yet I am pretty sure people will continue to use elevators, and those elevators will be serviced. These revenues will continue as long as elevators are in use.

There are a number of businesses like this. They all act as a kind of “toll booth”. I keep going back to the idea of a physical toll booth, because infrastructure is hard to replicate — once it’s in, it’s in.

Luxury

I’ve yammered on about luxury endless times, so I’ll keep it brief. Luxury — at the top level — is insulated from usual consumer spending habits because they’re targeting the top 1% of spenders. It’s also useful here to think about the consumer imperative here: as fortunes are made with AI the human need to signal status remains the same. It has been the same since the industrialists of the North of England made huge fortunes; it has been the same since the robber barons of America made fortunes in the 19th century; it has been the same since merchants in Venice, during the Renaissance, imported goods and sold them at a hefty profit. The desire to signal status does not change.

Here are the latest results from Hermes. It is perhaps the most quantified statement of humanity’s desire for status I know of.

Is there anything to be scavenged in the tech wreckage?

A couple of ideas, which I've come to while thinking of a world where agent-to-agent transactions are commonplace.

Datadog (stock down 23% YTD). Datadog monitors security for cloud-based applications. If you have a world with more agents, making decisions all the time, you will still need logs of what happened because things can and will go wrong. Datadog is explicitly positioning itself as a monitor of AI-based decisions. It's speculative — but if they position themselves correctly — they could be the “source of truth” (ugh I hate that phrase) for the “new” internet.

Okta (down 16% YTD). Okta deals with identification and authorisation. If we are to move into a future where agents are completing tasks and transactions for us, obviously identity will become a key issue: the possibility of rouge agents is quite real. Much like Datadog, Okta acts as a “policy” tool. Many people smarter than me have written of the risks of AI agents going buck wild. Perhaps, within the selloff, there’s a little bit of opportunity?