Predictions for 2026

AI, Booze stocks, The Florida land boom, and more

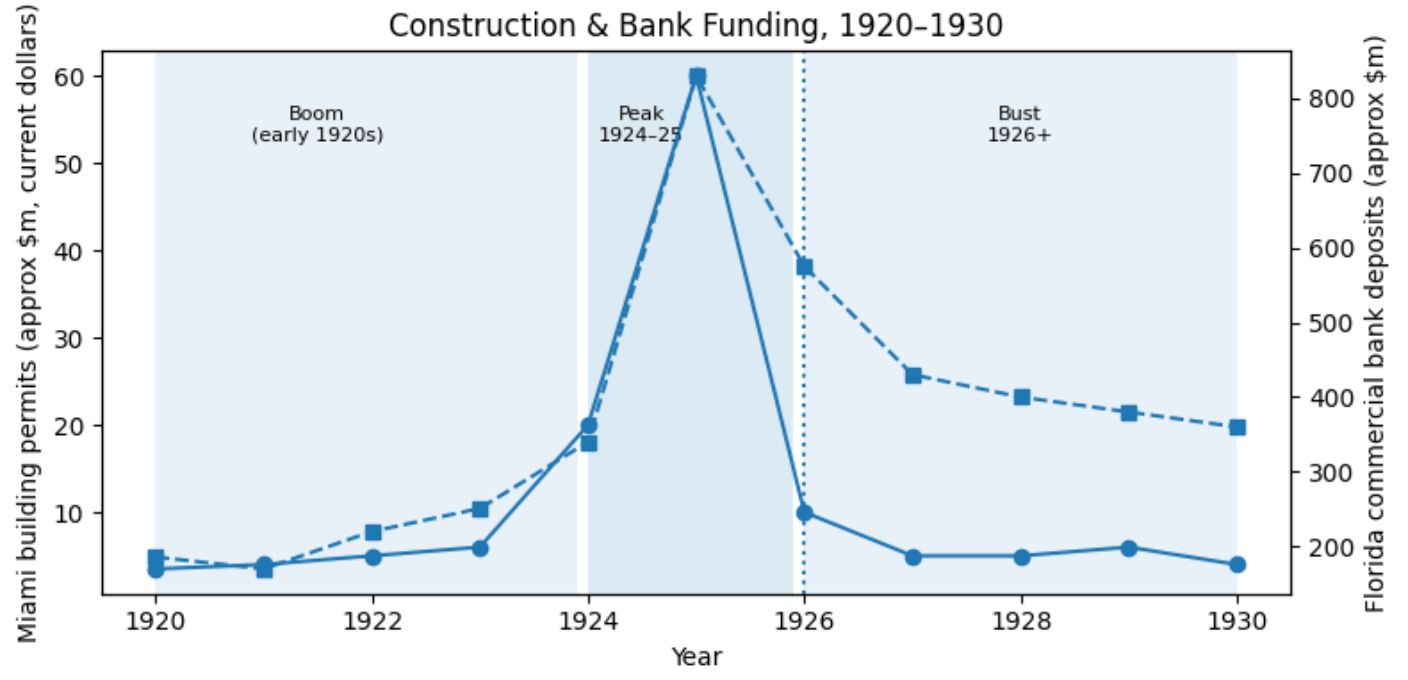

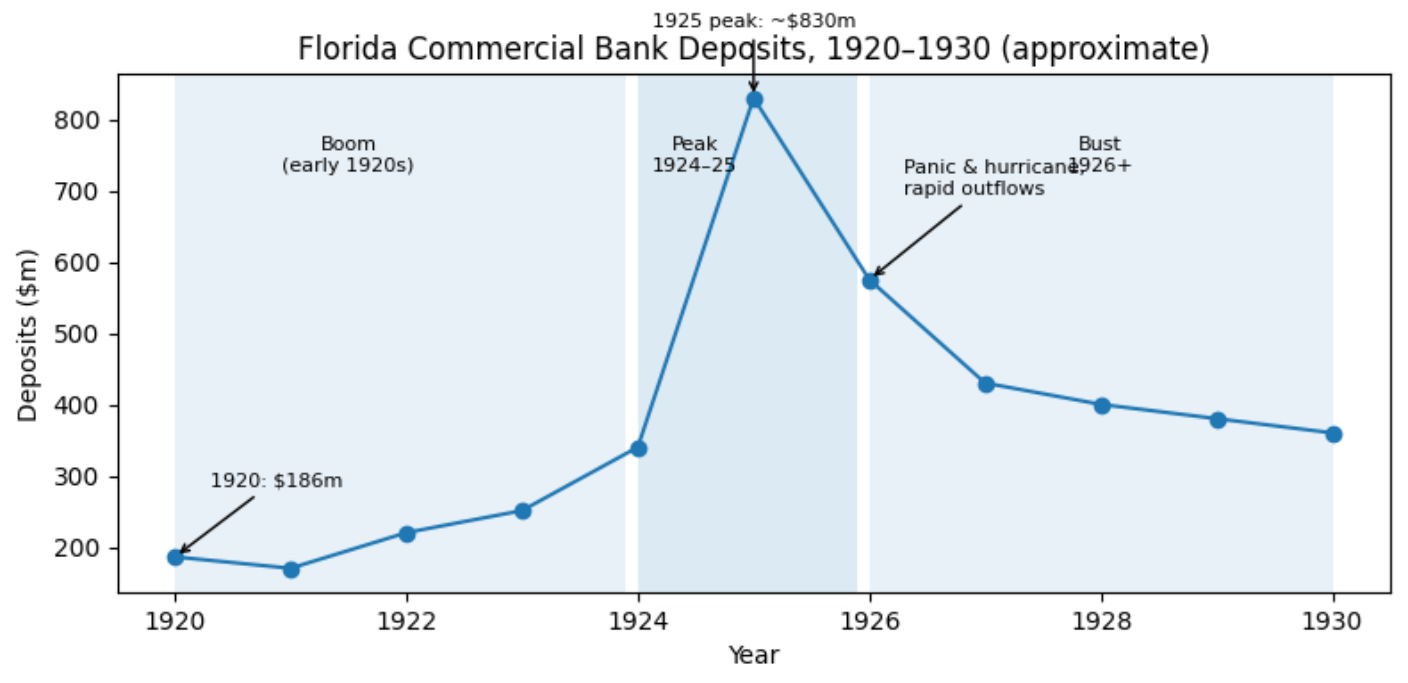

Well, it’s been a year, hasn’t it? I’m comforted by the thought that in the 1700s there were Italian merchants thinking the same thing who are long dead now; ditto ancient Romans and so on. Or if we go back a mere century there were plenty of long-forgotten speculators who partook in the Florida Land Boom, driven by the arrival of railways, cheap land, and (worst of all) an almost total ignorance of the harsh weather patterns of Florida, which led to many homes being built right in the eye of two hurricanes that ended the boom — the Miami hurricane of 1926 in particular.

Point is, life goes on, long-forgotten economic events happen, and we’re all really here for a short time. So don’t take it too seriously! And don’t take the following predictions too seriously. After all, I’m just an idiot at a keyboard!

But peruse the following charts, and keep in mind the cycles of boom to bust. Florida’s just one example…

So. Let’s talk about the next boom-to-bust story? Now we’ve had a little history lesson on Florida.

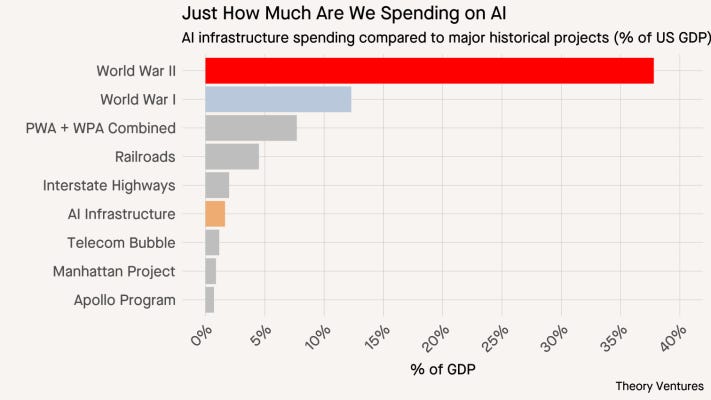

1) The AI boom goes bust

It’s important here that I’m not bagging AI technology. Rather, I’m concerned at the % of GDP spent on AI. With the exception of the two world wars, AI spend sits just behind the US’ total spend on railroads and highways.

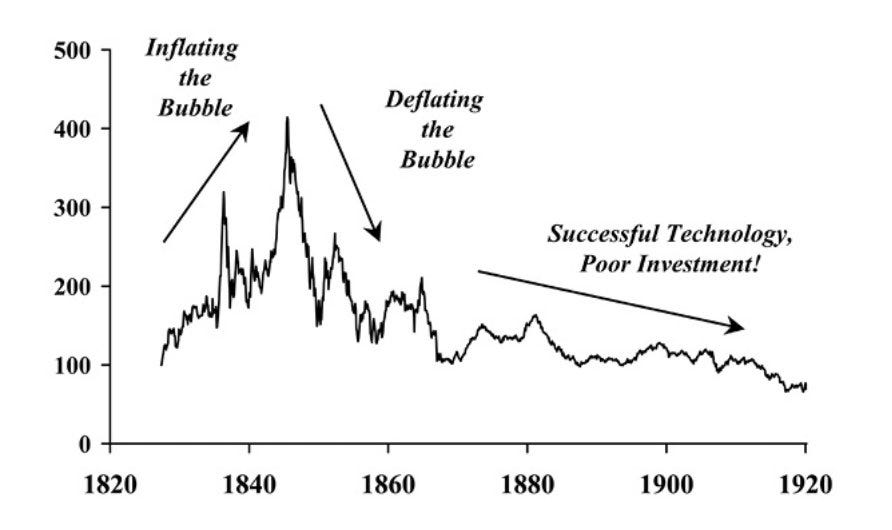

Same idea with AI. It’s a great technology, but a poor investment. If you turn your head to British railway bubble, you can see a similar pattern — great tech, poor investment:

I don’t know what the catalyst for the bubble bursting will be — I still think of the remarkable success of DeepSeek and its proof you can build a model a lot more cheaply than what was previously assumed. I also think about the market’s assumption that NVIDIA will take in $800b in revenue in the next five years. That’s eight hundred billion. I just think with valuations like that, who needs much of a catalyst? Camel’s back and all that…

2) The consumer continues to hurt

This is another “duh” moment, but I think a lot of the consumer’s pain has been hidden as markets continue to soar (largely because of AI/the mag 7/etc). Here in NZ the govt has done a remarkably poor job of navigating the economy — unemployment continues to rise, or just walk down the street and look at all the closed up shops. The same is echoed in actual countries that matter. Major consumer companies — Unilever, McDonald’s, Starbucks etc have already “sqouze” all they can out of pricing to protect margin. As the great Yogi Berra once said, ‘you can observe a lot just by watching’.

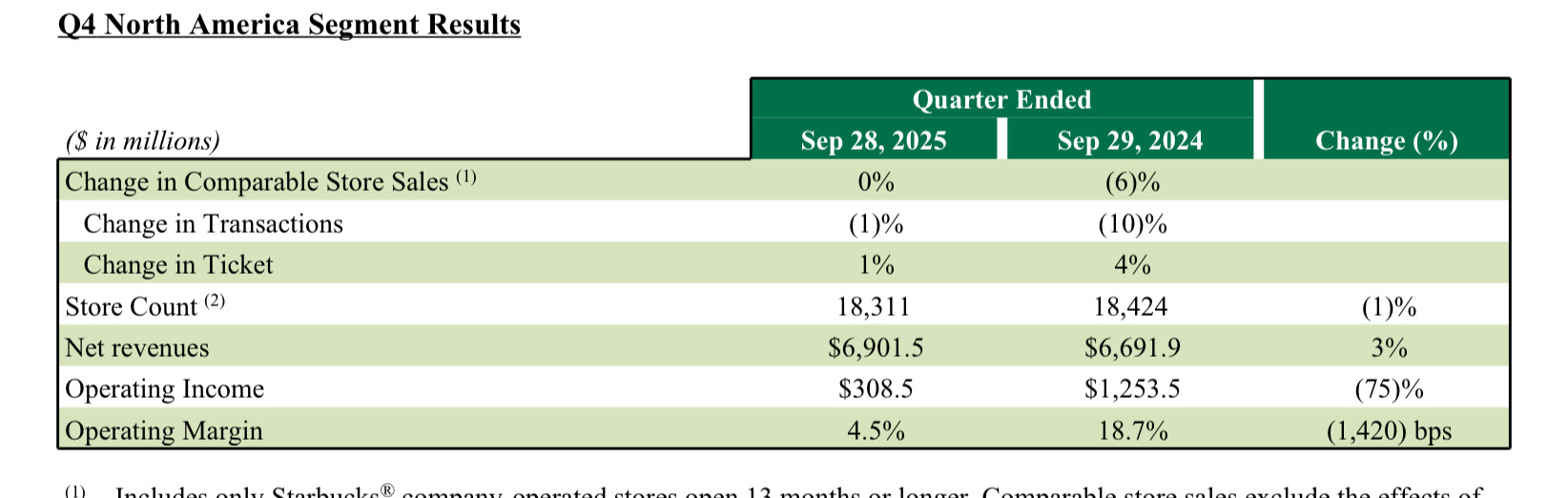

I wanna use Starbucks to really hammer in my point. Here’s Starbucks latest quarter; “ticket” is code for “how much we increased price by”; if you compare to the year before you can see that mgmt were able to squeeze prices 4% to offset transactions. This year they managed a mere 1%. This is a sign that mgmt knows the consumer is stressed, and there’s very little pricing power left in the pot.

On a macro basis — US unemployment sitting at 4.6%; UK at 5.1%; Eurozone 6.4%.

I’m more dubious of macro — I prefer indicators like Starbucks (note that operating margin too!) because that’s a real interface between the consumer and what they consume.

3) The hidden buy now pay later bubble

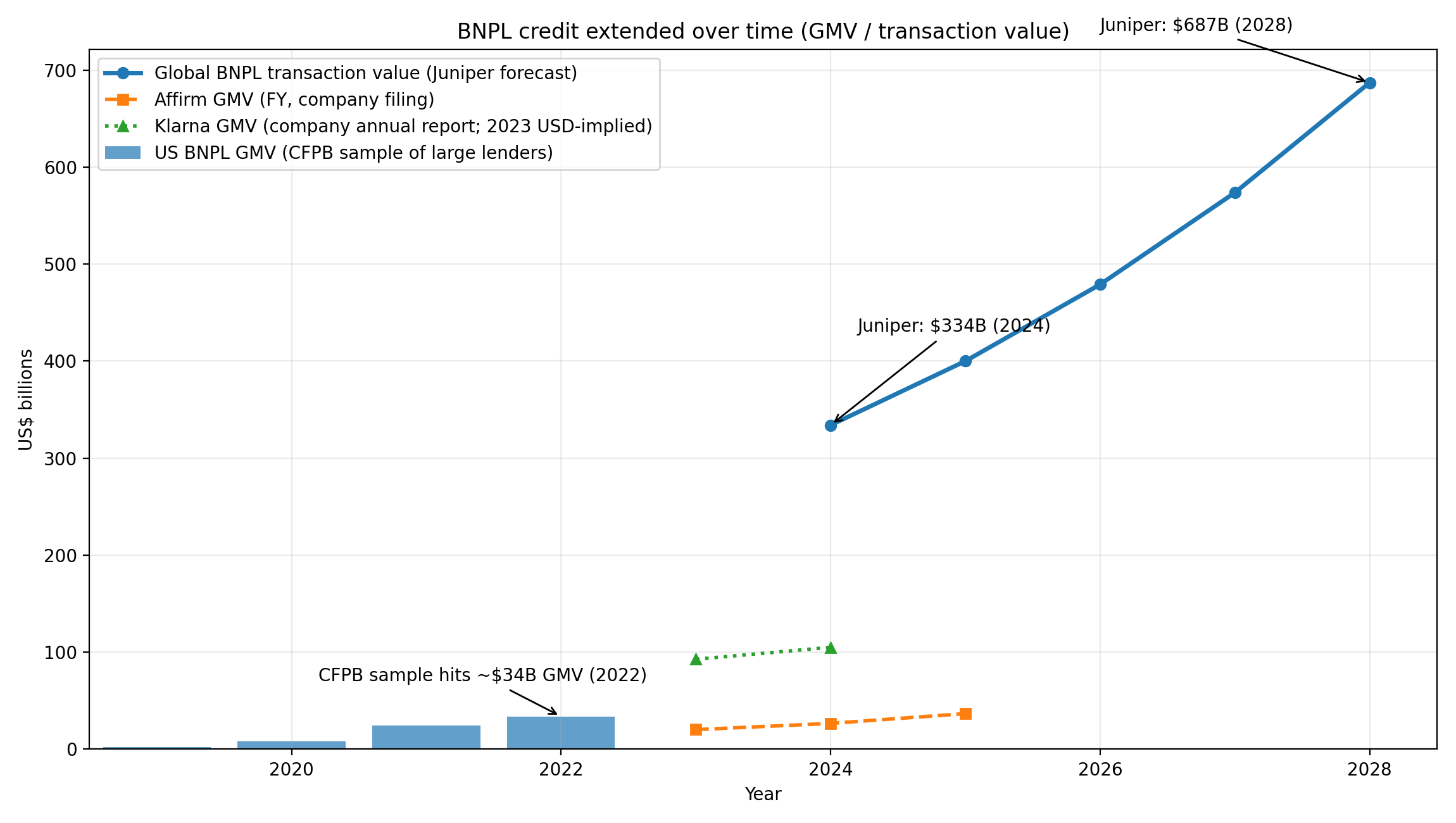

It used to be easy to understand how screwed the consumer was. FRED in the US provides a lot of data as to delinquent credit card debt, etc. Buy now pay later is more opaque. Often the providers don’t actually hold the debt at all, rather they sell tranches of the debt off to private credit providers, who sometimes package those tranches up and sell them to investors.

Does this remind you of anything?

Just to give you an idea of how big the market is, consider this data below from Juniper Research’s recent report — the BNPL market has exploded in recent years (and Affirm/Klarna give you very little solid data). Consider that a 4-5% delinquency rate implies ~$30b or so in defaults.

4) Expect more consolidation

Ya’ll know I spend a lot of time thinking about media and fashion. Here's a list of stocks that hold media assets that have not yet been acquired:

Lionsgate (LION), Starz (STRZ), Canal+ (CAN), Live Nation (LYV).

Given that there’s a lot of appetite for Warners, it seems to me that these much “smaller” companies are the last of their kind. If you’re Comcast (Hulu), Disney, Paramount Skydance or yes, Netflix…well, you’d be looking at these, wouldn’t you?

Turning to fashion, I expect it to be more of a game of musical chairs. Expect Kering to continue to sell underperforming brands (looking at their hard luxury segment), while Richemont remains a company that owns Van Cleef and Cartier and then a bunch of irrelevant stuff — owner/Chair J Rupert is not getting any younger. Perhaps brands Richemont owns, like Chloe and Alaia, would do better under another company?

5) Quiet luxury is dead

This one doesn’t need much of an explanation. It was dead last year, it’s even more dead now. Consider Blazy’s latest Chanel collection - held on a NY subway — it’s bold, brash, almost wilfully ugly at times and reminds me of SATC (for the economics head, note that hemlines are low … if you’re a subscriber to hemline theory, you'll know that implies recession).

6) NZ small caps stay winning

NZ small caps handily beat NZX large caps this year. Same story again. Plenty of acquisition targets — AoFrio, Rakon (heard that one before…), The Warehouse (on the basis of their RE portfolio alone), Oceania Healthcare. I have very little excitement for our large caps, except perhaps Gentrack.

7) The return of booze (it never went away)

My conviction trade last year was luxury. It's done well — Kering up +60%, etc. The basis of it was real simple. These companies had been sold off due to a few quarters of weak results, fears on consumer spending in China, and a few poor capital allocation decisions (looking at Kering in particular — with the purchase of luxury perfumery Creed for +$1b — the company sold it to L’Oreal and is now getting their house in order).

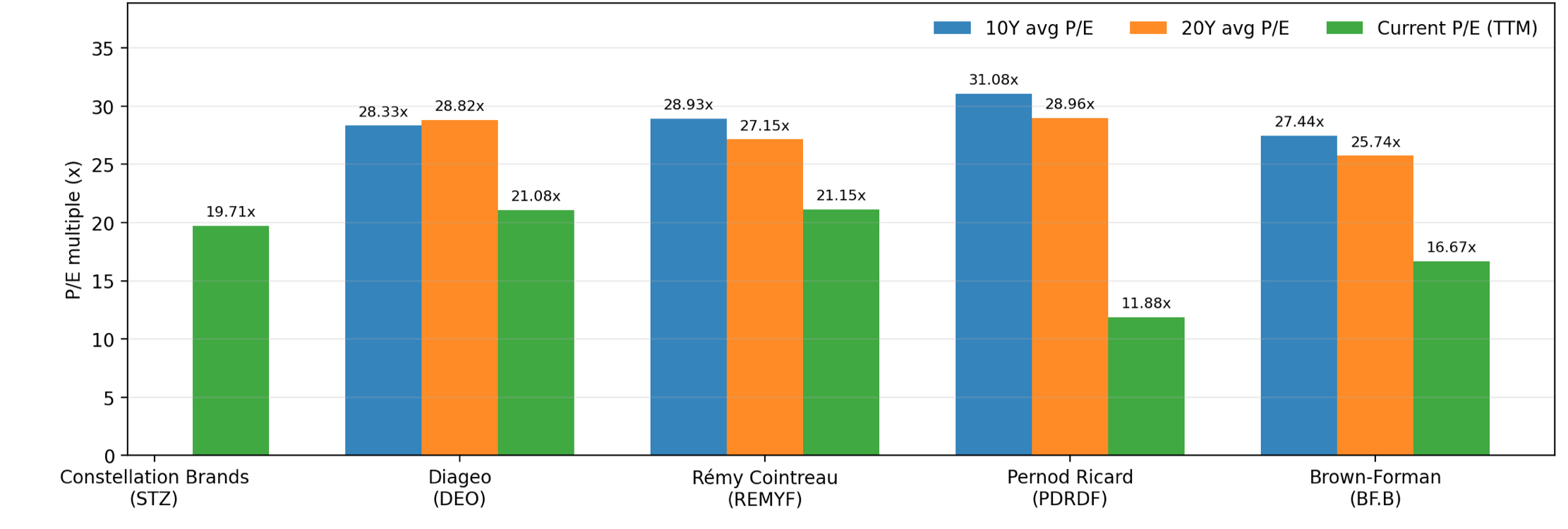

Stocks that have not done well this year are ye olde booze stocks. They are all trading well below their average historical price to earnings multiple, on both a ten year and twenty year basis.

Now you might say: but Eden, people are drinking less! And I will say: we’re facing a recession, do you really think people are going to go through it sober? Do you think they’re going to put on a goddamn mindfulness podcast and go to sleep while they can't pay rent? It’s a cynical bastard thing to say, I know, but it’s hard to not look at the discounts on offer here and think — ok, there’s some value to be had.

“But Eden!” I hear you say. Don’t you know half these companies are structurally in poor shape?

Sure I do. So was Kering a year ago. As I’ve said before, I don’t expect wild growth from any of these companies (there’s a reason I chose 10 yr and 20 yr P/Es — they “even out” the COVID bump). Nor do I expect them to re-rate to their previous multiples. But c’mon, we’re just talking value here. Booze stocks are at the bottom of the market in terms of pessimism. I don’t particularly like Pernod (though, given they hocked off their underperforming Aussie wine assets, they’re probably in a better position than they were…), but 11x earnings it just looks stupidly cheap — the market is implying either significantly less earnings for the next few years, or it believes Pernod only has eleven or so years left of life. I find this implausible.

As I've said before, I don’t have any special insight into the booze industry. I am still a dyed-in-the-wool Munger acolyte, and I think 1) people will continue to drink 2) the big boys continue to enjoy significant economies of scale and 3) the market is incredibly pessimistic on these stocks, as Buffett says…be greedy when others are fearful.