Endeavouring onwards

Endeavour, Penfolds, and Estée Lauder

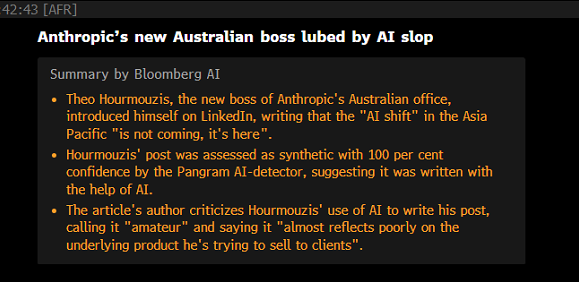

Presented without comment… new Anthropic NZ/Aus boss uses AI to write LinkedIn post…gets called “Lubed” by Bloomberg.

Hopefully the embarrassment of this will stop the deluge of AI generated “thought leader” slop I see when I dare to look at LinkedIn… it’s a hellscape out there, alongside Facebook (one Q I do have is: do the boomers using AI to write nonsense simply have no respect for writing? Or do they think nobody can tell? I swear, if I see another “it’s not this, but that” sentence I will lose it).

Anyway, moving on.

Endeavour and “The Chief”

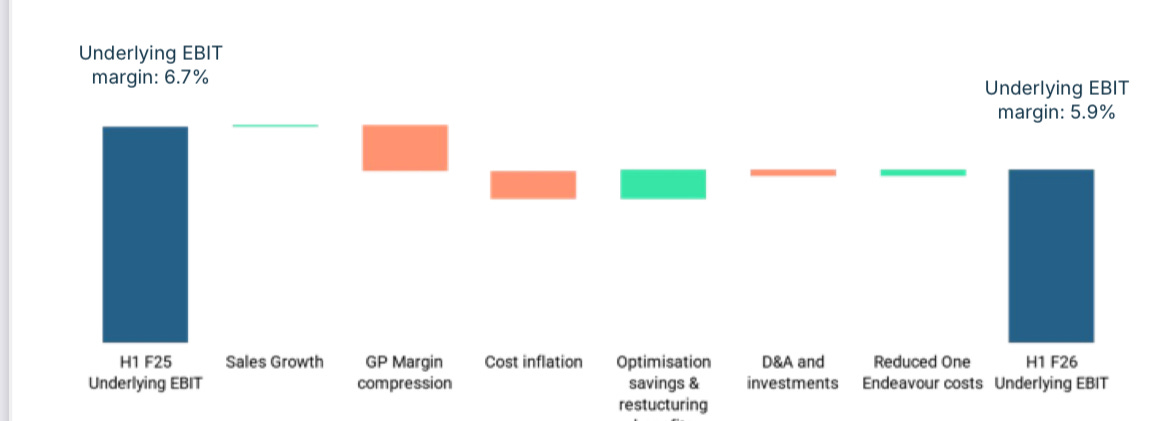

It must suck to be Jayne Hrdlicka, the new-ish CEO of Australian booze giant Endeavour Group (or even more to be a long-suffering shareholder; shares are down 46% since the company demerged from former parent Woolworths). The booze giant (they own Dan Murphy’s, etc, and pubs, presumably relying on the magic of the pokies) reported fairly weak results — yes, retail grew 2.9%, but every analyst worth their salt knows that includes Easter and Anzac Day sales. Sales, adjusted for those one-offs, were flat.

You have to think of the shareholders who went in for the ride when Endeavour was demerged — I guess roughly at the right time — the COVID boom, etc. But yet if the buying of alcohol and all that is a bellweather for the Aussie economy, it doesn’t look too good. She’s targeting $100m of savings (sure, ok) and stockpiling fast moving items (increasing inventory by $400m). All of this seems ok — albeit stockpiling +$400m more of inventory seems a little risky?! But is it enough to move the needle? See below from their HY presentation…retail ebit margins are getting squeezed like a watermelon…

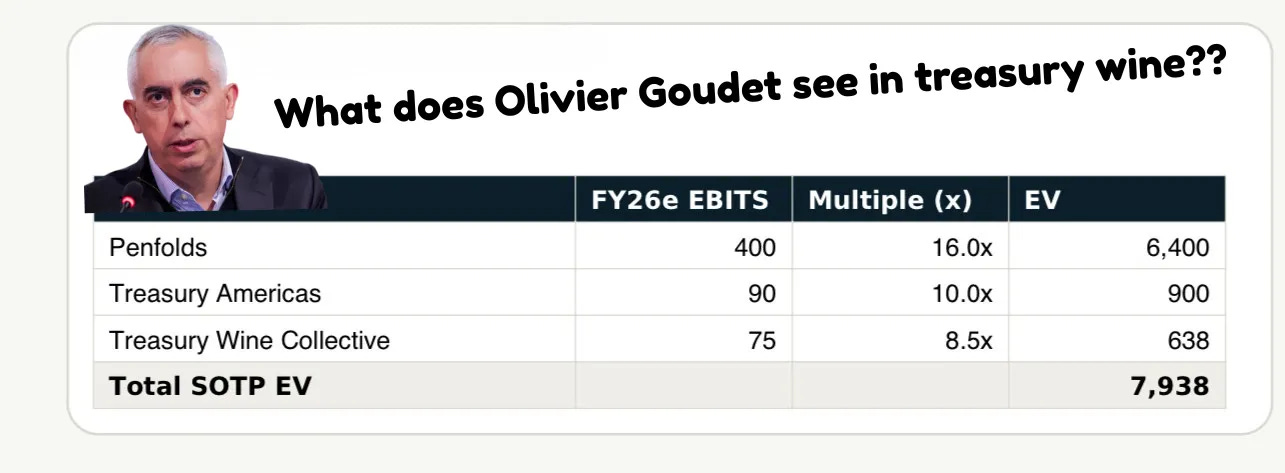

A similar thing is going on at Treasury Wine Estates. You can think of Treasury as “Penfolds” and everything else (i.e a sea of shit). I did a little bit of math on Treasury some time ago, when the former “genius” behind JAB (that’s sarcasm) took a stake. See below.

Also, you have Robert Foye, the former COO of Treasury and CEO of Accolade weighing in. Foye calls himself “The Chief”. Unironically. He is THE CHIEF. He’s been pushing for a change at Treasury, has offered his services as a non-exec director, called for a board shakeup and also posts videos like this on YouTube. I wish I was joking.

I mean, if you are the former CEO of a Very Big Australian booze company, is it a good idea to subject the internet (or all 387 people who watched it) to your daily routine? Does anyone really want to look into Foye’s eyes, as he stares into the mirror like a kind of middle aged narcissus?

It’s a little disturbing. But at least he has a cat?

The point is — you’ve got “the chief” pushing from a change, both via his videos, seminars and constant AFR communication (I guess Street Talk loves him), and you’ve also got Olivier Goudet with his 6.71% stake.

My point at the time was Penfolds is probably worth something; the rest of the company is worth a great deal less. Clearly Treasury management knows this — they have just merged Penfolds back to being “in house”, meaning an offer for the brand would be considerably more complicated. Think of it like taking someone hostage (Penfolds in this case), and saying “if you want this you’ll have to buy the rest of our shit too, 'struth!”

I think this is an interesting move in itself. Goudet had signalled he bought because he saw value in the luxury brands, i.e. Penfolds. Goudet also no doubt has the backing to make a whole offer for Penfolds. And now he can’t — at least easily. In the meantime, Treasury is down 19% YTD.

Has Gentrack lost its shine?

I’ve been keeping at eye on Gentrack for a long, long time. I remember when it traded at +$11.00! Gentrack must be one of NZ’s few software success stories (save Xero, obviously). The company provides cloud-native software solutions, billing systems, and CRM tools for utility companies and airports. It’s deeply boring. Stock trading below $5.00 as of writing — a “mere” 25x earnings. Mgmt expects revenue to be flat; signalled a buyback; stands by their medium term target of +15% CAGR (stand by your man…).

Also, this line:

We have taken the strategic decision to prioritise growth and global leadership over short term EBITDA.

As you know, the NZ market (and Aussie market) doesn’t like phrases like these. You get mgmt teams who do everything they can to make EBITDA look as good as possible and often come up with the dreaded “adjusted EBITDA” which is, of course, bullshit.

Here’s the rub, though — Gentrack has still not announced any meaningful new tier one customers. So — while it’s nice and all to prioritise growth — how do you get there without adding on tier one customers?

In other words, you’re looking at a previously hyper-growth company now a little in the doledrums. Oh dear. Maybe at $3.00 it’s good value…

Estée Lauder

As you know, I’ve had a bit of a preoccupation with Estée Lauder for a while. If you believe the headlines, the company had a good quarter! But dig in further and you’ll see a bunch of the “adjusted” earnings which strip out restructuring costs.

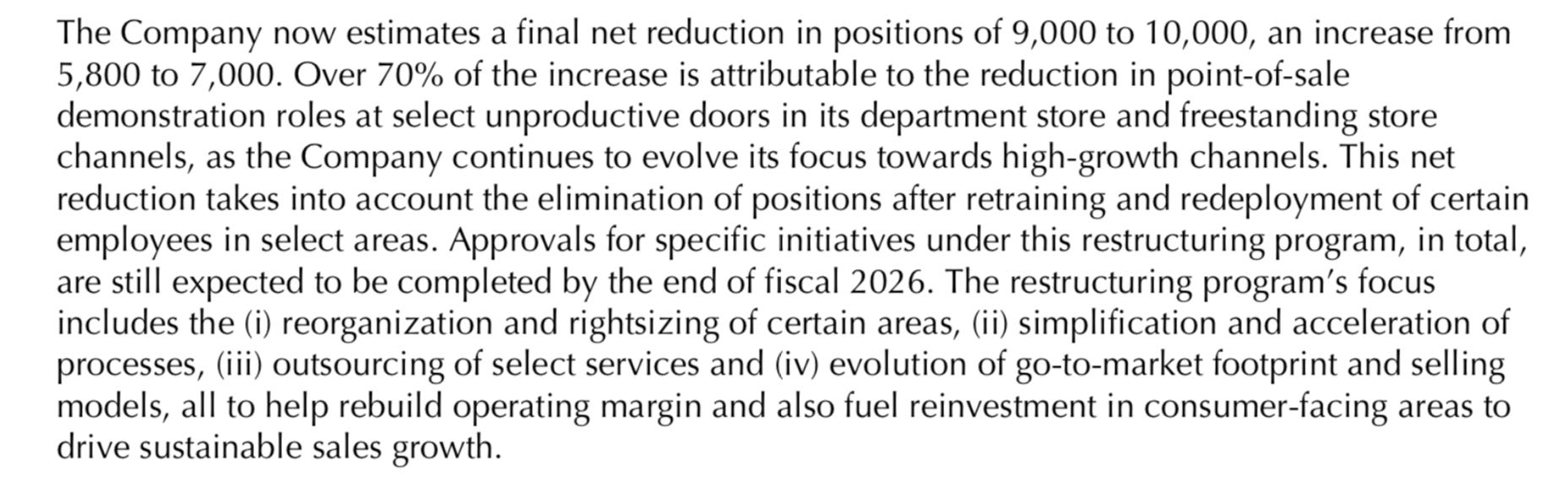

It gets worse — skincare sales were flat; makeup sales were flat; hair care sales were flat, with the only bright spot being fragrance (+10%). Most of the margin improvement — which is illusory anyway, because restructuring costs are real — came from the company’s continued workforce elimination. There’s this interesting paragraph:

Translation: we’ll cut a bunch of point of sale roles, especially those product demonstrators in department stores, and we’re going to sell more stuff on Amazon and at Ulta.

The danger here should be pretty obvious. Estée Lauder prides itself on having a bunch of mid-to-high market brands (MAC, Tom Ford, etc). Point of sale demonstrators are a key marketing component, just as Apple “Geniuses” were in the early days of the Apple Store. By moving your sales to Amazon, etc, you’re i) at the mercy of Amazon’s pricing power and ii) eroding any branding/loyalty you can build in-store and “flattening” your brand to compete with everyone else.

I’m reminded of Nike’s disastrous DTC strategy, which was similar. It doesn’t work. Simply put, to have a premium product you need evangelists. Amazon is not an evangelist. Nor is Ulta. And that’s the thing — when you get rid of your evangelists, you’re looking at a one-way path down to purgatory.